-

File Your Taxes

Find a Location

Find a Location -

Resolve Tax Issues

Resolve Tax Issues

Resolve Tax Issues

-

Tax Resources

See all Tax Help

Tax Tools

Tax Tips & Resources

-

Log in | Sign up

Log in | Sign up

JH Accounts

|

|

Oh no! We may not fully support the browser or device software you are using ! To experience our site in the best way possible, please update your browser or device software, or move over to another browser. |

IRS FORMS: FORM 8880

Claiming the Saver’s Credit for Retirement and ABLE Account Contributions with Form 8880

Published on: February 26, 2021

What is IRS Form 8880? Learn about Form 8880 and claiming the Saver’s Credit for Retirement and ABLE account contributions.

What is Form 8880 used for?

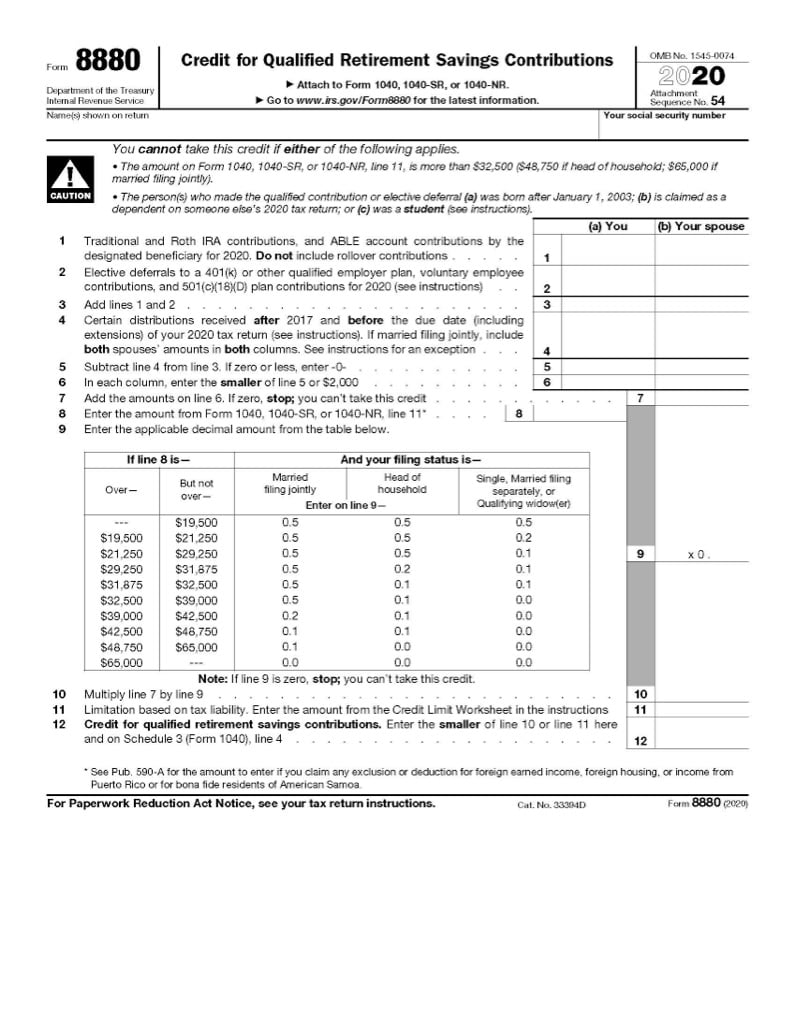

Form 8880 is used to compute the credit for qualified retirement savings contributions, also known as the "Saver's Credit." This credit is designed to incentivize low- and moderate-income taxpayers to save for retirement, and disabled persons to build savings with ABLE accounts.

Married taxpayers who file jointly can use Form 8880 to report contributions made by both the taxpayer and spouse, rather than filing separate forms. The nonrefundable tax credit is worth 10%, 20%, or 50% of up to $2,000 of contributions based on filing status and income based on a phaseout range (for a maximum credit of $1,000).

What are the income limits for the Saver’s Credit?

For 2020, the following income limits apply to the Saver's Credit based on filing status:

- Single, married filing separately, and qualifying surviving spouse: up to $32,500

- Head of household: up to $48,750

- Married filing jointly: up to $65,000

In addition to income limits, taxpayers who can be claimed as another taxpayer's dependent or were a student in 2020 cannot claim the credit. You are considered a student if you were enrolled as a full-time student at a university or technical or trade school or received full-time farm training from a school or government agency. Correspondence schools, digital learning, and job training do not count.

What types of retirement plan contributions are eligible?

Voluntary contributions to the following plans are eligible for the Saver's Credit:

- Traditional and Roth IRAs

- 401(k)

- 403(b)

- 457(b)

- SEP plans

- SIMPLE plans

- Federal Thrift Savings Plan

- 501(c)(18)(D) nonprofit plans (can be found in Box 12 of Form W-2)

- Achieving a Better Life Experience (ABLE) accounts for eligible disabled persons, if the taxpayer is the designated beneficiary

Employer matches and other employer contributions are not eligible, only contributions from the taxpayer or their spouse in the applicable column. Contributions also must be voluntary, which they are not for certain public employee pensions like 414(h) plans. Subsequently, non-voluntary plan contributions do not qualify for the Saver's credit.

Is the Saver’s Credit affected by retirement plan distributions?

If you or your spouse received distributions from your retirement plans or ABLE accounts within the past three years, not just the open tax year, you will need to reduce your contribution amount by these distributions. Sometimes, this effectively nullifies the Saver's Credit.

Rollovers, loans from plans treated as a distribution, distributions from inherited IRAs as a non-spouse beneficiary, and distributions from military retirement plans will not reduce or nullify the credit amount.

The Saver’s Credit is nonrefundable, which means there is a limit on the credit allowed based on the total tax liability. If the Saver’s Credit exceeds their tax liability, the excess portion is lost and will not be refunded, carried into future tax years, or carried back to prior tax years.

About the Author

Jo Willetts, Director of Tax Resources at Jackson Hewitt, has more than 35 years of experience in the tax industry. As an Enrolled Agent, Jo has attained the highest level of certification for a tax professional. She began her career at Jackson Hewitt as a Tax Pro, working her way up to General Manager of a franchise store. In her current role, Jo provides expert knowledge company-wide to ensure that tax information distributed through all Jackson Hewitt channels is current and accurate.

Because trust, guarantees, convenience & money all matter

-

TRUSTED GUARANTEES.

Be 100% certain about your money & your taxes, year after year.

-

NATIONAL PRESENCE. LOCAL HEART.

We’re in your neighborhood & inside your favorite Walmart store.

-

40+ YEARS. 65+ MILLION RETURNS.

The kind of trusted expertise that comes with a lifetime of experience.